June 2024

|

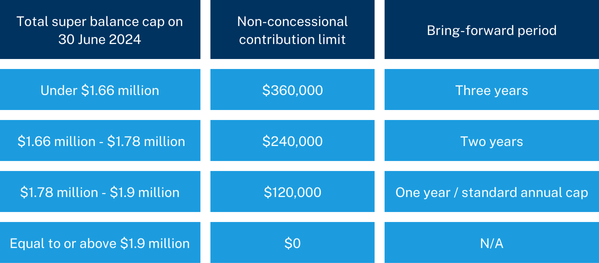

For the first time in three years, both the concessional and non-concessional caps will increase on 1 July 2024. As a result, from 1 July 2024:

The non-concessional contribution caps and threshold are summarised in the table below: |

It’s important to note that while higher caps can be beneficial, individuals should consider their overall financial situation to understand how these changes impact their retirement planning goals and tax position.

Should you wish to arrange a meeting to discuss these changes and how they impact your personal situation, please don’t hesitate to contact our Wealth Advisory team on 03 9325 6300 or info@matsteer.com.au.