This year’s Federal budget was widely expected to include significant tax changes compared to the reasonably moderate tax changes we have seen recently (with the exception of time limited COVID-based concessions). It did not disappoint.

The changes to capital gains tax, taxation of trusts and to a lesser extent negative gearing represent a fundamental change to the way in which business and investment has been structured for at least the last 20 years and even since capital gains tax was introduced back in 1985.

Combinations of discretionary trusts paired with trading and wealth companies have largely become the structure of choice for most small and medium family businesses looking to create and protect their wealth. These structures will now require a radical rethink and planning to transition to a tax effective structure which meets the future needs of the business, the owners and their families.

Your Matthews Steer advisor is well placed to assist you through this transitional period and make sure your business and wealth structure is adapted to the changes when they commence in 2027 and 2028.

Business Insights

Small and medium businesses

New minimum tax for discretionary trusts from 1 July 2028

From 1 July 2028, trustees will pay a minimum tax of 30% on the taxable income of discretionary trusts.

Beneficiaries, other than corporate beneficiaries, will receive non-refundable credits for the tax payable by the trustee. Corporate beneficiaries will be assessed on trust income but will be unable to claim a credit for the tax payable by the trustee.

The minimum tax will not apply to other types of trusts such as fixed and widely held trusts (including fixed testamentary trusts), complying superannuation funds, special disability trusts, deceased estates and charitable trusts.

Some types of income, such as primary production income, certain income relating to vulnerable minors, amounts to which non-resident withholding tax applies, and income from assets of discretionary testamentary trusts existing at announcement will also be excluded.

The Government will provide expanded rollover relief for three years from 1 July 2027 to support small businesses and others that wish to restructure out of discretionary trusts into another entity type, such as a company or a fixed trust.

Loss carry-back for companies

For tax years commencing on or after 1 July 2026, companies with aggregated annual global turnover of less than $1 billion will be able to carry back a tax loss and offset it against tax paid up to two years earlier. Loss carry back will apply to revenue losses only and will be limited by a company’s franking account balance.

Refundability of losses for start-up companies

The Government will also introduce loss refundability for small start‑up companies. For tax years commencing on or after 1 July 2028, start‑up companies with aggregated annual turnover of less than $10 million that generate a tax loss in their first two years of operation will be able to utilise the loss to generate a refundable tax offset. The offset will be limited to the value of fringe benefits tax and withholding tax on wages paid in respect of Australian employees in the loss year.

Permanent extension to the small business asset write-off

From 1 July 2026, the Government will permanently extend the $20,000 instant asset write‑off for small businesses with turnover up to $10 million. Assets valued at $20,000 or more can continue to be placed into the small business simplified depreciation pool. The provisions that prevent small businesses from re‑entering the simplified depreciation regime for 5 years after opting out will continue to be suspended until 30 June 2027.

Optional monthly Pay as You Go Instalments

From 1 July 2027, small and medium businesses will be able to opt in to reporting and paying PAYG instalments monthly and to using an ATO-approved calculation embedded in accounting software to calculate and vary their instalments. This is stated as supporting businesses by enabling tax instalments to better reflect real time business activity. Taxpayers with a demonstrated history of non‑compliance will be required to report and pay PAYG instalments monthly.

Electric Car FBT discount

From 1 April 2029, a permanent 25% discount on fringe benefits tax (FBT) will be available for all electric cars valued up to and including the fuel‑efficient luxury car tax threshold, implemented through a 15% per cent rate in the FBT statutory formula. This will replace the current FBT exemption. As a transitional measure:

- all electric cars valued up to $75,000 provided before 1 April 2029 will retain their FBT exemption; and

- electric cars provided between 1 April 2027 and 1 April 2029 valued between $75,000 and the fuel efficient luxury car tax threshold will be eligible for the 25% discount on their FBT cost.

Large business and international

Large businesses and multinationals can breathe a sigh relief as the focus has been overwhelmingly on domestic investor taxes (CGT discount, negative gearing and trusts). Large international businesses are more affected by ongoing integrity measures, compliance tightening and targeted foreign investor rules that were previously announced.

Strengthening Foreign Resident Capital Gains Tax (CGT) Regime

In the 2024-25 Budget, the Government had announced that it would strengthen the foreign resident CGT regime. Draft legislation (Foreign CGT Regime legislation) has now been released in respect of these announcements.

In particular, the draft legislation is designed to close loopholes so foreign residents pay CGT on a broader range of Australian assets (e.g. indirect interests in land-rich entities, mining and infrastructure assets beyond just direct land). These changes include retrospective elements and may impact past transactions particularly relating to infrastructure assets that taxpayers may have thought as not being subject to CGT.

Renewable Energy Asset Discount

The abovementioned Foreign CGT Regime legislation also introduces a temporary 50% CGT discount for in respect of foreign investment into certain investments in the Australian renewables energy sector.

The temporary CGT discount is targeted at foreign institutional investors and applies to CGT events that happen from commencement until 30 June 2030.

Pillar 2 Rules – Side by Side Package

The 2026-27 Federal Budget included only a minor update to the already enacted Pillar 2 rules with proposed amendments to Australia’s Pillar 2 legislation to align with the OECD’s “Side-by-Side” (SbS) package (agreed in January 2026) for consistency with other jurisdictions. This applies from 1 January 2026.

Broadly, the SbS package means US headed multinational groups can elect certain SbS safe harbours with reduced exposure to certain Australian top up taxes but with Pillar 2 filing obligations remaining unchanged.

ATO Counter Fraud Strategy

The Federal Government announced further funding and powers for the ATO to focus on strengthening tax system integrity, modernising fraud prevention and targeting non-compliance.

The funding will be $86.3m over four years from 1 July 2026 plus $9.7m per year ongoing 2030-31.

The measures will also strengthen the ATO’s ability to:

- combat fraud by tax agents and other intermediaries

- be given powers to pause the recovery of tax debts of taxpayers who are victims of fraud by tax intermediaries, and waive those debts in appropriate circumstances, and to recover the debts from the tax intermediaries

- Existing garnishee powers to be expanded to include jointly held assets in certain circumstances.

The ATO will undertake additional targeted compliance activities over the two years from 2026–27 to address fraud in the system further, including in relation to the Research and Development Tax Incentive.

The measures are projected to increase tax receipts by $218m with an emphasis on implementing modern technology for real-time prevention, victim support and stronger support against intermediaries and high-risk behaviours.

R&D, Innovation and Grants

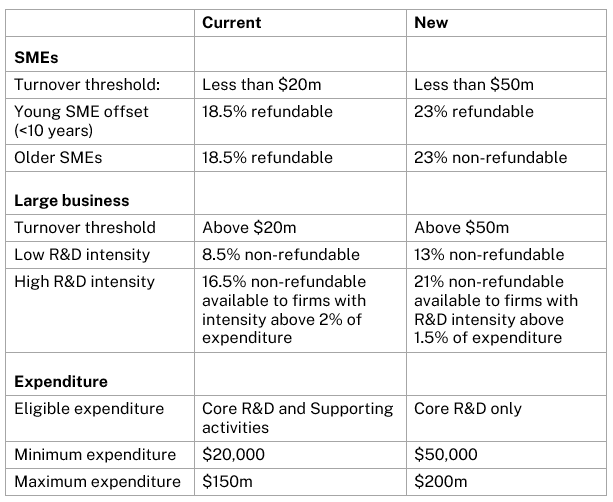

Research and Development Tax Incentive

There are significant changes ahead for the R&D tax incentive that will create waves in the R&D community and present some interesting transitional challenges. The major changes are summarised below.

Summary of R&DTI offset changes from 1 July 2028 onwards:

The most contentious change is the exclusion of supporting activities from eligibility. This will create challenges around defining the boundaries between core and supporting activities and increase the compliance burden on claimants.

Restricting the refundable R&D offset to companies younger than 10 years, no matter whether the company has previously claimed or not, will also create many losers.

Venture Capital Tax Incentives

The Government will expand the venture capital tax incentives to better facilitate venture capital investment and support early stage and growth businesses. From 1 July 2027:

- The venture capital limited partnership (VCLP) cap on the asset size of the investee business at the time of investment will be increased to $480 million, from $250 million

- The early stage venture capital limited partnership (ESVCLP) cap on the asset size of the investee business at the time of investment will be increased to $80 million, from $50 million

- The ESVCLP tax incentive cap on the asset size of the investee business, at which investment returns can be fully tax exempt, will be increased to $420 million, from $250 million

- The maximum fund size of ESVCLPs will be increased to $270 million, from $200 million.

The increases will apply to new and existing funds and to new investments they make, including where funds make further investments in businesses already held. ESVCLPs must remain in compliance with their existing investment plans or seek approval for a replacement plan.

The eligible venture capital investor program will be closed to new applications from 7.30PM (AEST) 12 May 2026.

Other relevant budget innovation provisions:

- Australia’s Economic Accelerator grant program that supported commercialisation of university research has been cut saving $759.9 over the next 5 years

- $508.5 million to increase disbursements for medical research from the Medical Research Future Fund.

- $70 million for ‘AI Accelerator’ grants to boost AI development through the CRC and CRC-P programs.

Australian families and individuals

The budget provides further tax support for workers through a tax offset and standard tax deduction. However, as expected, the most significant changes are to capital gains tax and changes to negative gearing for residential properties.

The budget provides wholesale tax changes to capital gains tax and negative gearing, the scale which have not been seen for many years.

Here we highlight some of the key tax measures affecting Australian individuals and families.

Capital gains tax

From 1 July 2027, the Government proposes to replace the 50% capital gains tax (CGT) discount for individuals, trusts and partnerships with cost base indexation and a 30% minimum tax rate on capital gains.

For eligible CGT assets:

- Assets acquired and disposed of before 1 July 2027 will remain fully subject to current CGT rules

- Assets acquired on or after 1 July 2027 will be taxed entirely under the new regime

- Assets held before 1 July 2027 and sold after that date will be subject to transitional treatment, with gains accrued up to 1 July 2027 taxed under existing rules and gains accruing thereafter taxed under the new rules. There is no tax impact until the asset is disposed of.

For transitional assets, the 50% CGT discount will apply to the gain between the original cost base and the asset’s value at 1 July 2027. Gains accruing from that date will be calculated using indexation, with the asset’s 1 July 2027 value effectively treated as a new cost base. The post 1 July 2027 net gain will be taxed at a minimum of 30%.

The 1 July 2027 value may be determined either by obtaining a valuation or by applying a prescribed apportionment formula. It is not clear on what basis this apportionment will be determined but Treasury information indicates the ATO will be providing a calculator to assist taxpayers looking to use the apportionment formula instead of a valuation. It is also not clear what form of valuation will be accepted. For example, will a director’s valuation be sufficient for an unlisted private company value?

Pre‑CGT assets will remain exempt for gains accrued before 1 July 2027, with the new rules applying only to gains accrued after that date. This is a fundamental change for the currently completely exempt CGT assets.

It does not appear that companies will get the benefit of any cost base increase on account of indexation. This may create a tension between restructuring to a company in light of some of the other announced Budget changes.

The are some specified exemptions. They are:

Assets exempted

- For new residential premises, the investor can choose between the current CGT 50% discount and the new indexed cost base with a minimum 30% tax. This asset class will be defined as new builds which genuinely add to the supply. This will include dwellings on vacant land and demolished properties where replaced with a greater number of dwellings. New builds cannot have previously been sold, unless first owned by the builder and not occupied for more than 12 months.

- Qualifying affordable housing, which will continue to attract a 60% CGT discount.

Investors exempted

- Superannuation funds including SMSF. Long-term investment gains on assets held for more than 12 months by superfunds will continue to attract a 33% discount.

- Recipients of income support payment recipients, including Age Pension recipients will be exempt from the minimum tax.

Related matters to note

- There will be no change to the Small Business CGT Concessions, perhaps increasing the importance of these concessions where available.

- Treasury has indicated that the impact of this for the tech and start up sector has not yet been worked through. Importantly, Treasury has referred to the “unique characteristics” of this industry as a reason to further consult on the interaction of these capital gains tax reforms with incentives for investment in early-stage and start-up businesses. One such area may be in relation to the ESS start-up concessions as these changes may render them redundant.

Negative Gearing Changes

As expected, the budget includes measures to remove negative gearing benefits on residential properties acquired after Budget night (7.30pm AEST 12 May 2026), unless it relates to new builds. The changes will apply to residential properties acquired after Budget night but only come into effect from 1 July 2027.

Currently, investors are allowed to deduct a net rental loss from a negatively geared residential property against other taxable income. Negative gearing will continue to be available for residential properties acquired (or contracted) before Budget night.

From 1 July 2027, for residential properties acquired after budget night, net rental losses will be able to be carried forward to offset residential property income in future years (including future capital gains from residential properties).

Negative gearing will continue to apply to new builds. The exemption for new builds is intended to support investment in new builds to increase housing supply.

These changes will apply to individuals, partnerships, companies and most trusts. Widely held trusts, and superannuation funds (including SMSFs) will be excluded.

The changes are limited to residential property and don’t apply to other negatively geared investments (such as commercial properties or shares).

Further exemptions to the negative gearing changes will be available for private investors who support government housing programs.

$250 Working Australians Tax Offset

The Federal Government has announced a new tax cut for working Australians through the introduction of the $250 Working Australians Tax Offset (WATO), which will apply from the 2027–28 income tax year.

The offset will provide a permanent annual tax offset of up to $250 for eligible taxpayers on income derived from work. This includes wages and salaries, as well as net business income earned by sole traders. The Working Australians Tax Offset will increase the effective tax-free threshold for income derived from work by nearly $1,800 to $19,985 (or up to $24,985 for workers eligible for the Low Income Tax Offset).

The Working Australians Tax Offset is scheduled to commence on 1 July 2027.

$1,000 instant tax deduction

The government will continue a push to legislate a standard $1,000 deduction for Australian tax residents who earn income from work, starting 1 July 2026. If introduced, eligible Australians will be able to claim the deduction without needing receipts for work-related expenses.

This will still allow some deductions to be claimed in addition to the instant tax deduction, including investment expenses, charitable donations and union and professional association membership fees.

Taxpayers must choose either the $1,000 standard deduction or to claim their actual work‑related expenses. If actual expenses exceed $1,000, they may choose to claim those instead, subject to normal substantiation rules.

Previously announced tax cuts

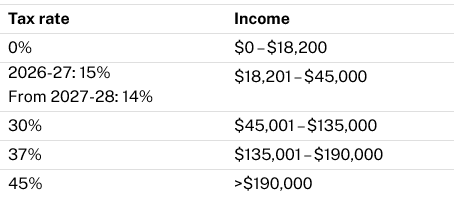

The income tax cuts announced in last year’s budget have been legislated and will begin to apply from 1 July 2026.

From 1 July 2026, the 16% tax rate (which applies to taxable income between $18,201 and $45,000) will be reduced to 15%. From 1 July 2027, this tax rate will reduce to 14%.

For individuals with taxable income of at least $45,000, this equates to a tax saving of $268 per year in 2026-27 and $536 per year from 2027-28.

The tax brackets and rates, excluding the 2% Medicare levy, for the current financial year and those that will apply up to and from 1 July 2027 are shown below.

Increasing Medicare levy low-income thresholds

The Government will increase the Medicare levy low‑income thresholds by 2.9% for singles, families, and seniors and pensioners from 1 July 2025.

Strengthening Medicare

The budget includes an additional $2.1 billion over 5 years to ensure access to quality primary and specialist healthcare through Medicare Urgent Care Clinics and increased access to bulk billing.

Boosting home ownership

The budget will provide $2 billion over four years from 2027 Housing Support Program – Local Infrastructure Fund which provides support to local governments and utility providers to expedite delivery of housing enabling infrastructure.

Retirement and Superannuation

The 2026 budget has largely left superannuation unchanged, although the confirmation of exclusion from the CGT and negative gearing changes was welcome.

What will affect superannuation in the coming year will be the increase in contribution caps from 1 July 2026, the introduction of Pay Day Super, as well as Division 296 legislation finally being passed earlier this year for those with balances over $3 million.

SMSFs excluded from changes in CGT and negative gearing

The widely discussed and now confirmed changes to the CGT discount and negative gearing have now been announced. It has been confirmed that SMSFs are excluded.

Increase in contribution caps

Although not mentioned in this budget, there are a number of contribution caps set to rise from 1 July 2026.

- The standard concessional contribution cap, which includes employer, salary sacrifice and personal contributions for which an individual can claim a personal tax deduction, will increase from $30,000 (in the 2025 and 2026 financial years) to $32,500 from 1 July 2026.

- The non-concessional contribution (NCC) cap will increase from $120,000 to $130,000 from 1 July 2026. This also means that the maximum non-concessional cap, available under the bring-forward provisions, will increase from $360,000 to $390,000.

- The Super Guarantee rate remains at 12%, from 1 July 2025, with no further change.

Division 296 additional tax on high superannuation balances

Separate to the Budget, the Government passed legislation earlier this year regarding Division 296 to reduce tax concessions to individuals with a Total Superannuation Balance (TSB) exceeding $3 million. This is now set to take effect from 1 July 2026.

To summarise, individuals with a TSB in excess of $3 million and $10 million will be subject to an additional tax on earnings of 15% and 10% respectively. These thresholds will be indexed over time. The tax is calculated by using an updated version of an adjusted earnings calculation (which no longer includes unrealised market movements), multiplied by the percentage of the member’s balance over the relevant threshold.

There will also be the ability to choose to uplift the cost base of your SMSF assets to the market value at 30 June 2026. This will only be for the purpose of calculating Division 296 only, and the standard tax calculation for income tax with apply for capital gains.

Pay day super

Also starting from 1 July 2026, employers must pay superannuation at the same time they pay salary and wages to employees. This will give employees greater visibility and control over their superannuation entitlements and assist the ATO in recovering unpaid superannuation.

If you would like to discuss how recent budget announcements may affect your business or investment decisions, please reach out to your Matthews Steer advisor or Contact us to be put in touch with the right person for your needs.

May 2026 – Sandie Boswell